Autus Newsletter » Autumn Budget 2025

Personal Taxation

Income tax

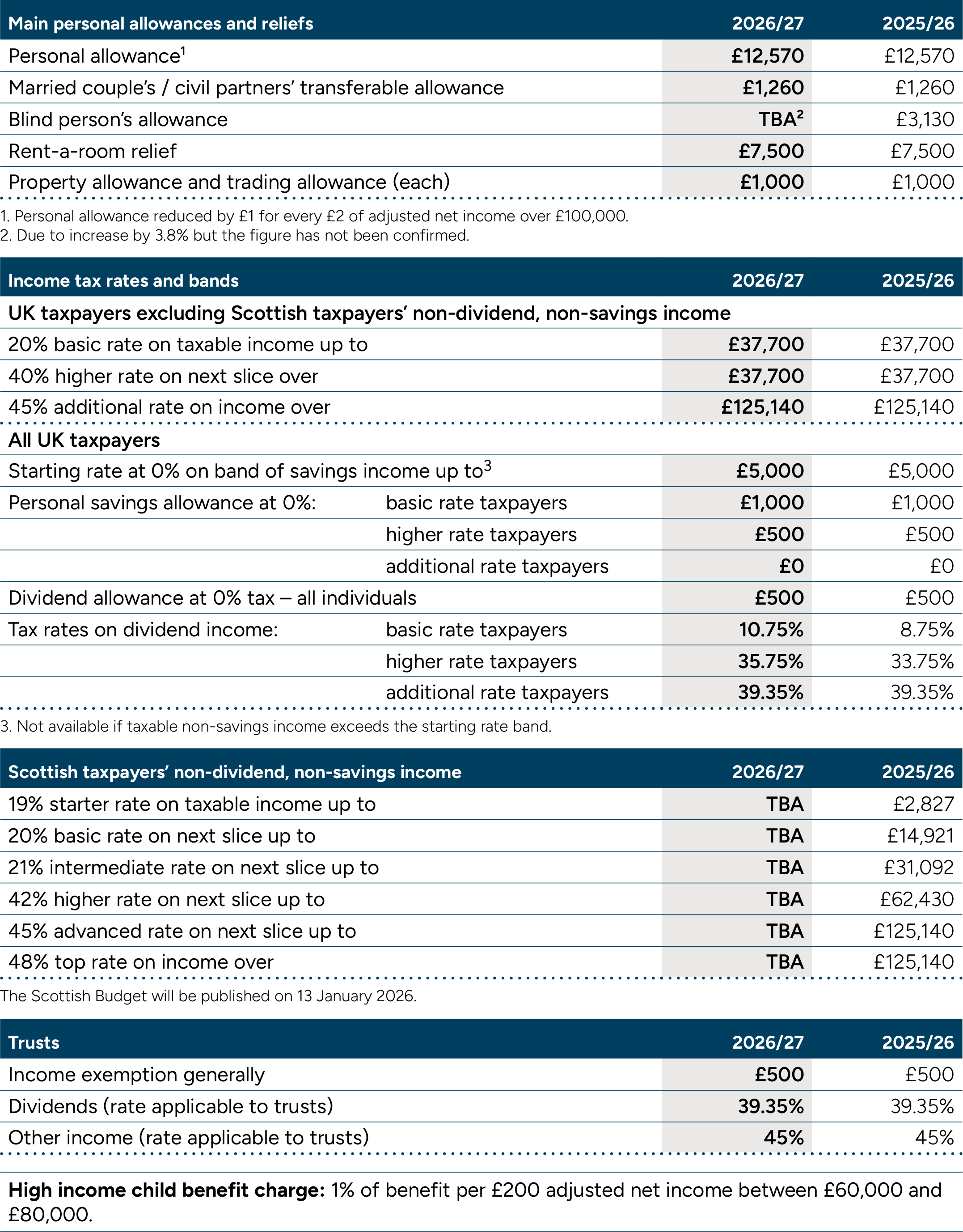

The personal allowance for 2026/27 will remain at £12,570, the higher rate threshold will stay at £50,270 and the additional rate threshold at £125,140. The freeze to these thresholds will be extended for another three years, up to and including 2030/31.Savings rate band

The 0% band for the starting rate for savings income for 2026/27 will remain at its current level of £5,000.Dividend tax

The ordinary and upper rates of tax on dividend income will rise by two percentage points to 10.75% and 35.75% from April 2026. There will be no change to the dividend additional rate of 39.35%. The dividend allowance will remain at £500 for 2026/27.Savings tax rate

From April 2027, the tax rate on savings income will rise by two percentage points across all tax bands to 22%, 42% and 47%.Property Income

A new set of tax rates will apply to property income from April 2027. The property basic rate will be 22%, the property higher rate will be 42% and the property additional rate will be 47%. The changes to property income rates will apply in England, Wales and Northern Ireland.The government will engage with the devolved governments of Scotland and Wales to provide them with the ability to set property income rates in line with their current income tax powers.

Ordering of income tax reliefs and allowances

The income tax rules will be changed from 6 April 2027 so that reliefs and allowances deductible in income tax calculations will only be applied to property, savings and dividend income after they have been applied to other sources of income.National insurance contributions (NICs)

The NIC thresholds for employees and self-employed individuals will be frozen at their current levels for a further three years from April 2028 to April 2031. The class 1 secondary threshold will also be held at its current level of £5,000 from April 2028 to April 2031.Access to pay voluntary class 2 NICs abroad will be removed from 6 April 2026. The period of initial residency or contributions required to pay any voluntary NICs outside of the UK will be increased to ten years.

The government will also launch a wider review of voluntary NICs with a call for evidence in the new year.

Car taxes

A new mileage charge for electric and plug-in-hybrid cars (PHEV) will come into effect from April 2028. Drivers will pay for their mileage alongside their existing vehicle excise duty (VED) at rates of 3p a mile for fully electric vehicles and 1.5p a mile for plug-in hybrids.From 1 April 2026, the threshold for VED expensive car supplement for new EVs will be increased by £10,000 to £50,000.

Planned changes to benefit-in-kind rules for employee car ownership schemes will be deferred until April 2030. For those still in contracts at that time, transitional arrangements will also be introduced to provide additional support.

With retrospective effect from 1 January 2025 until 5 April 2028 a temporary easement will apply to mitigate the increased benefit-in-kind tax liabilities of PHEV company cars due to new emission standards. Transitional arrangements will apply to certain vehicles until 5 April 2031.

High value council tax surcharge

A high value council tax surcharge (HVCTS) will be introduced in England from April 2028 for residential properties worth £2 million or more, based on updated valuations to identify properties above the threshold.The charge will start at £2,500 a year, rising to £7,500 a year for properties valued above £5 million and it will be levied on property owners rather than occupiers. Local authorities will collect the charge on behalf of central government.

Loan charge review

Individuals affected by the loan charge will have an opportunity to make a new settlement with HMRC following a review of the legislation by the government. The loan charge was introduced to counter widespread disguised remuneration schemes where taxpayers received loans from employers instead of taxable salary. The schemes failed and individuals faced very large tax bills.This newsletter is for general information only and is not intended to be advice to any specific person. You are recommended to seek competent professional advice before taking or refraining from taking any action based on the contents of this publication. The Financial Conduct Authority does not regulate tax advice, so it is outside the investment protection rules of the Financial Services and Markets Act and the Financial Services Compensation Scheme. The newsletter represents our understanding of the law and HM Revenue & Customs practice as of November 2025. Past performance is not a reliable indicator of future performance. The value of investments and the income from them can go down as well as up, and you may get back less than you invested. The value of tax relief depends upon your individual circumstances. Tax laws may change. The Financial Conduct Authority does not regulate Accountancy Services, Legal Services, Taxation Advice, Business Consultancy Services, Estate Agency Services and some forms of private banking and debt consolidation.