Autus Newsletter » Autumn Budget 2024

Personal Taxation

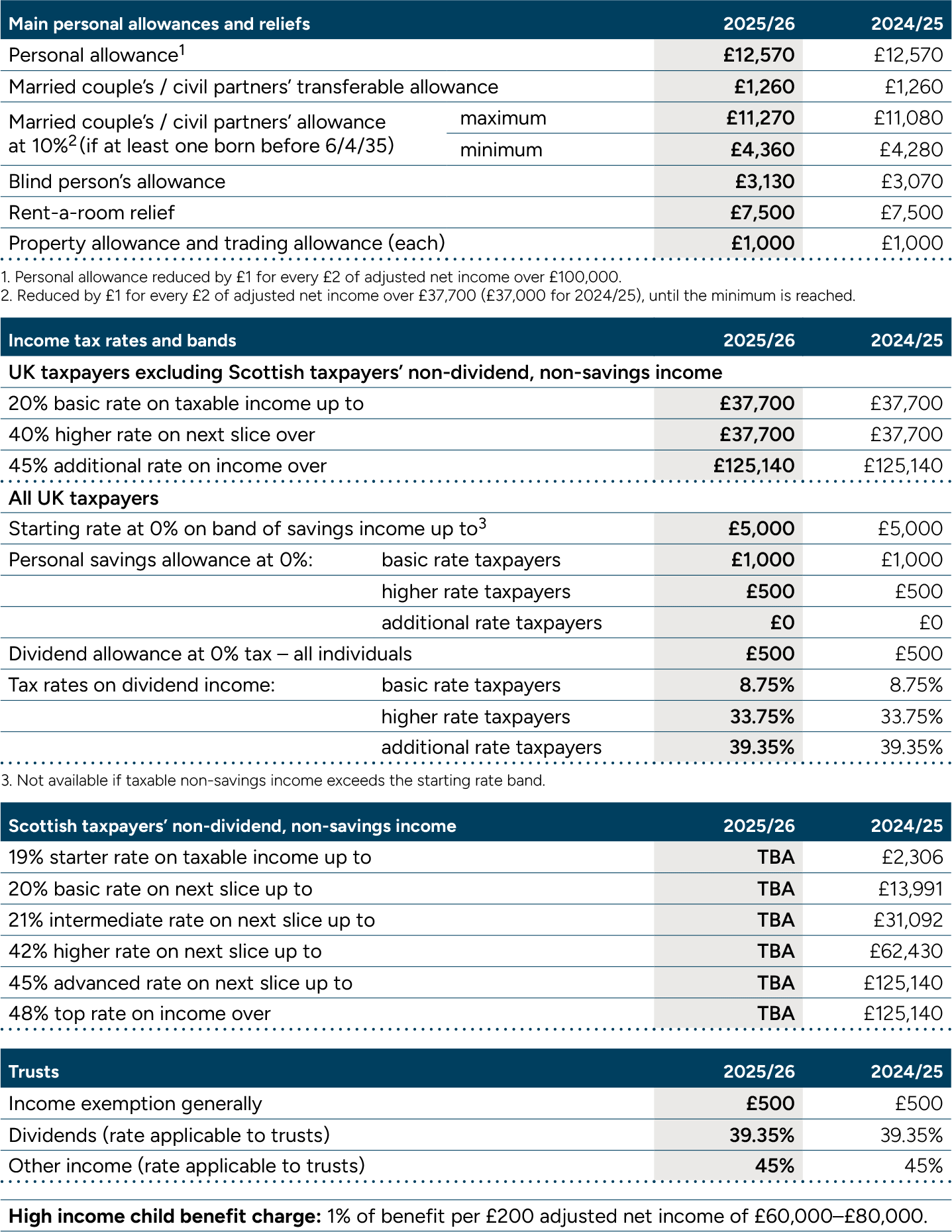

Income tax

The personal allowance for 2025/26 will remain at £12,570 and the higher rate threshold will stay at £50,270. The freeze on both will end from April 2028, when indexation will resume.Savings rate band

The 0% band for the starting rate for savings income for 2025/26 will remain at its current level of £5,000.Dividend tax

The dividend allowance will remain at £500 for 2025/26 and the rates of tax on dividends will also be unchanged.National insurance contributions (NICs)

The class 1 secondary (employer) contribution rate on earnings above the reduced secondary threshold (ST) of £5,000 will be increased from 13.8% to 15.0% from 6 April 2025. The employment allowance will rise from £5,000 to £10,500 for 2025/26 and the £100,000 upper threshold for eligibility will be removed. Employer NICs relief for hiring qualifying veterans will be extended to 5 April 2026.The ST will be reduced to £5,000 from 6 April 2025 until 5 April 2028 and be index-linked in line with CPI thereafter. The upper earnings limit, upper secondary thresholds and upper profits limit will remain aligned to the unchanged higher rate threshold at £50,270 for 2025/26. Similarly, the class 1 primary threshold of £12,570 will remain unchanged.

For 2025/26, the lower earnings limit will increase to £6,500 and the small profits threshold (SPT) will rise to £6,845. The upper earnings limit and class 4 upper profits limit will remain aligned to the higher rate threshold at £50,270 through to April 2028.

Class 2 contributions are no longer required from the self-employed, but those with profits below the SPT who wish to retain access to contributory benefits (e.g. state pension) have the option to make voluntary contributions at an increased rate of £3.50 a week for 2025/26. The voluntary class 3 rate will rise to £17.75 a week for 2025/26.

High income child benefit charge (HICBC)

The previous government’s proposal to base the HICBC on household incomes has been abandoned. Employed individuals will be able to pay their HICBC through their tax code from 2025, and self-assessment tax returns will be pre-populated with child benefit data for those not using this service.Company car tax

The company car tax rates for 2025/26 will generally increase. As announced in the Autumn Statement 2022, the appropriate percentage (AP) rates for electric and ultra-low emission cars will increase by one percentage point in each of 2025/26, 2026/27 and 2027/28. These will be subject to a maximum of 5% for electric cars and 21% for ultra-low emission cars.The rates for all other bands of vehicles will be increased by one percentage point for 2025/26 up to a maximum AP of 37%; they will then be fixed for 2026/27 and 2027/28.

For 2028/29 and 2029/30, the AP for zeroemission and electric vehicles will increase by two percentage points a year to 9%. For cars with CO2 emissions of 1-50g/km, including hybrid vehicles, the AP will rise to 18% in 2028/29 and to 19% in 2029/30. The APs for all other vehicle bands will increase by one percentage point a year in 2028/29 and 2029/30. The maximum AP will also rise by one percentage point each year to 38% for 2028/29 and 39% for 2029/30.

Changes to the taxation of non-UK domiciled individuals

The remittance basis of taxation for non-UK domiciled individuals will be replaced from 6 April 2025 with a residence-based regime. Individuals who opt into the new regime will not pay UK tax on any foreign income and gains arising in their first four years of tax residence. The previous government’s proposal of a 50% reduction in foreign income subject to tax in the first year of the new regime will not go ahead.For CGT purposes, current and past users of the remittance basis will be able to rebase personally-held foreign assets to 5 April 2017 on a disposal where certain conditions are met. A new residence-based system for IHT will be introduced from 6 April 2025, aimed at ending the use of offshore trusts (excluded property trusts) to shelter assets from IHT.

The temporary repatriation facility will be extended to three years, expanding the scope to offshore structures, and simplifying the mixed fund rules.

Overseas workday relief will be retained and reformed, with the relief extended to a four-year period and the need to keep the income offshore removed. The amount claimed annually will be limited to the lower of £300,000 or 30% of the employee’s net employment income.

Loan charge review

An independent review of the loan charge will be commissioned by the government. Further details will be set out in due course.@ Copyright 30 October 2024. All rights reserved. This summary has been prepared very rapidly and is for general information only. The proposals are in any event subject to amendment before the Finance Act. You are recommended to seek competent professional advice before taking any action on the basis of the contents of this publication.