Autus Newsletter » Autumn Budget 2024

Capital Taxes

Capital gains tax (CGT) annual exempt amount

The CGT annual exempt amount for individuals and personal representatives will remain at £3,000 for 2025/26. The annual exempt amount for most trusts will stay at £1,500 (minimum £300).CGT rates

The lower main rate of CGT will increase to 18% and the higher main rate will rise to 24% for disposals made on or after 30 October 2024.The rate for business asset disposal relief and investor’s relief (IR) will increase to 14% from 6 April 2025 and will increase again to 18% from 6 April 2026.

The lifetime limit for IR will be reduced to £1 million for all qualifying disposals made on or after 30 October 2024.

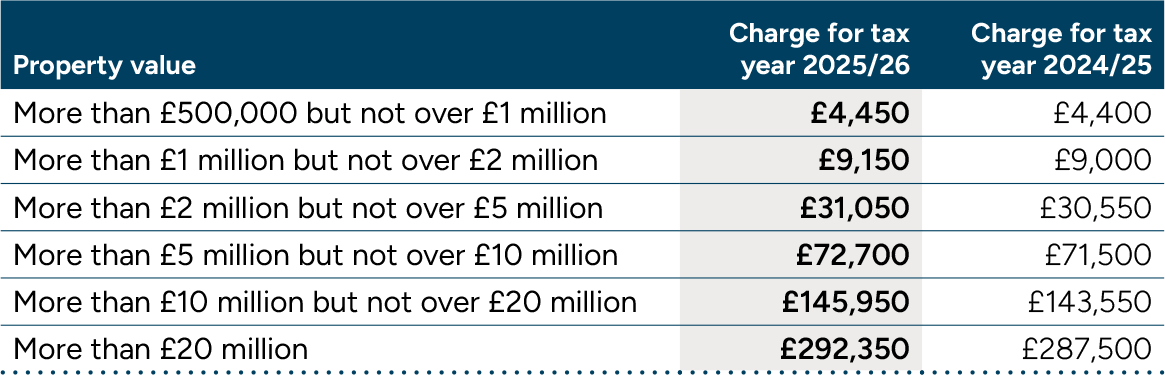

Annual tax on enveloped dwellings (ATED)

The ATED annual charge will rise by 1.7% from 1 April 2025 in line with CPI. For ATED filing and payment purposes in 2025/26, a property revaluation as at 1 April 2022 is required (or the date of acquisition for a property acquired after that date).

Carried interest

From April 2026, all carried interest, which is mainly held by individuals engaged in private equity and hedge fund businesses, will be taxed within the income tax framework and subject to class 4 NICs. There will be a 72.5% multiplier applied to qualifying carried interest that is brought within charge. As an interim step, the current two CGT rates for carried interest will both increase to 32% from 6 April 2025. There will be a consultation on introducing further conditions for access to the regime.Inheritance tax (IHT) bands

The existing freeze on the IHT nil rate band (£325,000), the residence nil rate band (£175,000) and its associated taper threshold (£2 million) will be extended by two years to 5 April 2030.IHT business and agricultural reliefs

From 6 April 2026, the current 100% rate of relief will continue for the first £1 million of combined agricultural and business property for individuals and trusts, except for shares designated as ‘not listed’ on the markets of recognised stock exchanges, such as AIM. The rate of relief will be 50% for such assets above the £1 million threshold and for all ‘not listed’ shares.The existing 50% rates of business and agricultural relief will continue where they currently apply (e.g. to farmland let before 1 September 1995) and will not be affected by the new allowance.

For certain trusts that were established before 30 October 2024, the £1 million allowance will apply to each trust. The £1 million allowance will be divided between trusts where a settlor sets up multiple trusts on or after 30 October 2024.

Extension of IHT agricultural property relief to environmental land management

From 6 April 2025, agricultural property relief will be extended to cover land managed under an environmental agreement with, or on behalf of, the UK government, devolved governments, public bodies, local authorities, or approved responsible bodies.

IHT on unused pension fund and death benefits

Unused pension funds and death benefits payable from a pension will be brought into a person’s estate for IHT purposes from 6 April 2027.Stamp duty land tax (SDLT)

From 31 October 2024, the higher rate for additional dwellings SDLT surcharge will be increased from 3% to 5%.The single rate of SDLT charged on the purchase of dwellings costing more than £500,000 by corporate bodies will also be increased by two percentage points to 17%.

As previously announced, the threshold of the 0% SDLT band for residential property will be cut from £250,000 to £125,000 from 1 April 2025. Between £125,001 and £250,000 a rate of 2% will apply.

The 0% band for first time buyers will be reduced to £300,000 from 1 April 2025 for properties valued up to £500,000.

@ Copyright 30 October 2024. All rights reserved. This summary has been prepared very rapidly and is for general information only. The proposals are in any event subject to amendment before the Finance Act. You are recommended to seek competent professional advice before taking any action on the basis of the contents of this publication.