Autus Newsletter » Spring Budget 2024

Capital Taxes

Capital gains tax (CGT) annual exempt amount

The CGT annual exempt amount for individuals and personal representatives will be cut to £3,000 for 2024/25. The annual exempt amount for most trusts will likewise fall to £1,500 (minimum £300) as previously announced. The allowance will no longer be index linked.From 6 April 2024, the higher rate of CGT for residential property disposals will be cut from 28% to 24% while the lower rate (for any gains that fall within an individual’s basic rate band) will remain at 18%.

Inheritance tax (IHT)

The IHT nil rate band will remain at £325,000 from 2024/25 to 2027/28, as previously announced. The residence nil rate band (RNRB) likewise stays at £175,000 and the RNRB taper continues to apply until April 2028 if the value of a deceased person’s estate is greater than £2 million.Payment of IHT

From 1 April 2024, personal representatives of estates will no longer need to have sought commercial loans to pay IHT before applying to obtain a ‘grant on credit’ from HMRC.Stamp duty land tax (SDLT): abolition of multiple dwellings relief

Multiple dwellings relief, a bulk purchase relief in the SDLT regime for England and Northern Ireland, will be abolished from 1 June 2024. Property transactions with contracts that were exchanged on or before 6 March 2024 will continue to benefit from the relief regardless of when they complete, as will any other purchases that are completed before 1 June 2024.

SDLT: first-time buyers’ relief for nominee purchasers

The rules for claiming first-time buyers’ relief from SDLT in England and Northern Ireland will be amended from 6 March 2024. Individuals (including victims of domestic abuse) who buy a leasehold residential property through a nominee or bare trustee will be able to claim first-time buyers’ relief. Before this change the individual was not treated as the purchaser and so was not entitled to the relief.Annual tax on enveloped dwellings (ATED)

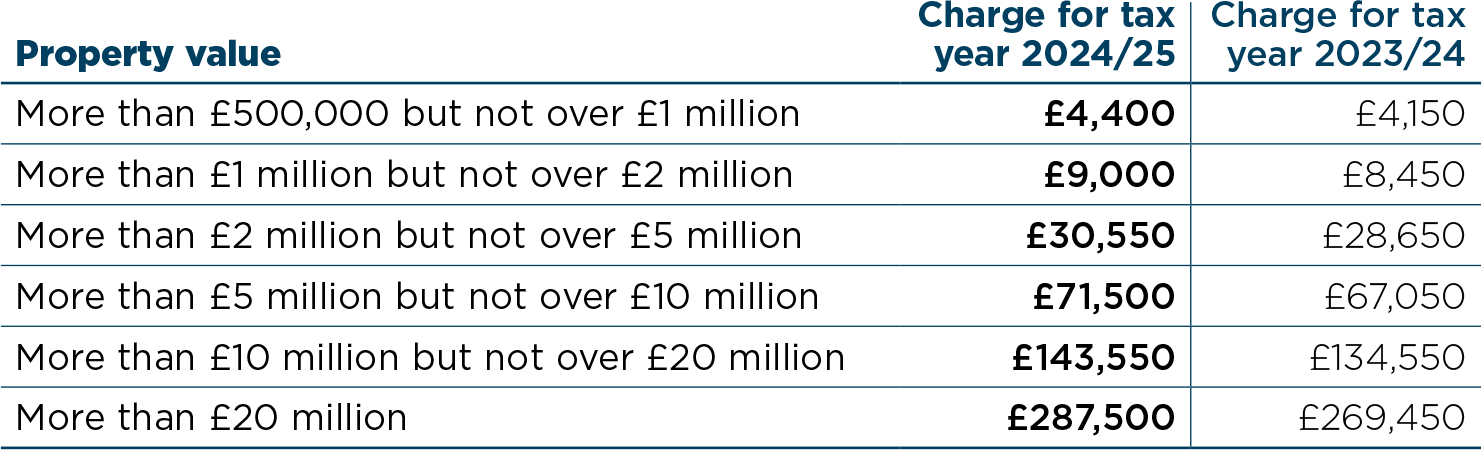

The ATED annual charge rises by 6.7% from 1 April 2024 in line with the CPI. For ATED filing and payment purposes in 2024/25, a property revaluation as at 1 April 2022 is required (or the date of acquisition for a property acquired after that date).

@ Copyright 6 March 2024. All rights reserved. This summary has been prepared very rapidly and is for general information only. The proposals are in any event subject to amendment before the Finance Act. You are recommended to seek competent professional advice before taking any action on the basis of the contents of this publication.