Capital Taxes

Capital gains tax (CGT) annual exempt amountThe annual exempt amount for individuals and personal representatives will remain at £12,300 until 5 April 2026, and the amount for most trustees will likewise remain at £6,150 (minimum £1,230).

Inheritance tax (IHT)The IHT nil rate band will remain at £325,000 until 5 April 2026. The residence nil rate band (RNRB) will likewise stay at £175,000 and the RNRB taper will continue to apply where the value of the deceased's estate is greater than £2 million.

THINK AHEAD - CGT reform remains on the agenda. Now may be a good time to review whether to realise your gains before the tax regime becomes harsher.

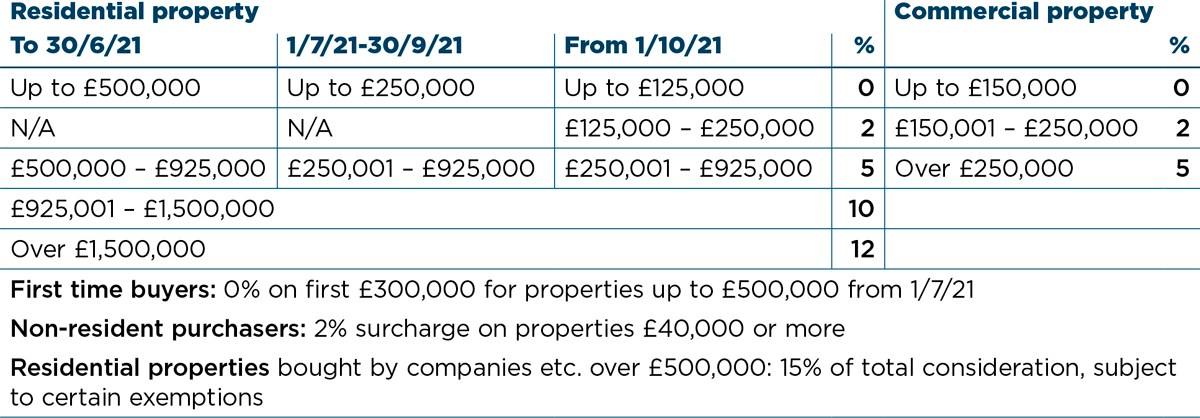

The temporary increase to £500,000 to the SDLT nil rate band for residential property in England and Northern Ireland is extended until 30 June 2021. From 1 July 2021 until 30 September 2021, the nil rate band will be £250,000 and will then return to £125,000.

Non-UK resident SDLTAs previously announced, there will be an SDLT surcharge on non-UK residents buying residential property in England and Northern Ireland from 1 April 2021. The surcharge will be 2% above the existing residential rates.

SDLT on slices of value (England & N Ireland)